What are Mutual Funds

Mutual funds are a collection of securities, such as stocks, bonds, options, or commodities that are pooled together into one fund.

Open ended funds have NAVs which stands for Net Asset Value.

This is calculated by dividing the total value of cash and securities within the portfolio, minus the liabilities, by the outstanding shares. This calculation is done at the end of each trading session.

Mutual funds do not trade though out the day like stocks, they are priced once a day.

Types of Mutual Fund Accounts

- Brokerage Account

- Mutual Fund Account

Diversification

The main advantage of investing is mutual funds is the diversification.

If an investor buys a single stock of an oil and that company goes bankrupt, the stock goes to zero and you lose your entire investment. This is called systematic risk.

Now If that same investor buys a mutual fund within the oil sector instead, and one of the companies within that fund goes belly up and declares bankruptcy.

The investor is better off since there are other individual stocks which represent individual companies that still have value. Thus, the investor does not lose the entire investment.

Professional Money Management

Professional money management can actually be considered either a pro or a con depending on the situation.

There are some mutual funds that have good track records, managed by good fund managers.

Morningstar is a website that provides plenty of detailed information about mutual funds for free, including the history of the fund managers that actually manage the fund.

Investors can order a prospectus from Morningstar, their broker or the mutual fund company itself in order to get the official documentation about the mutual fund.

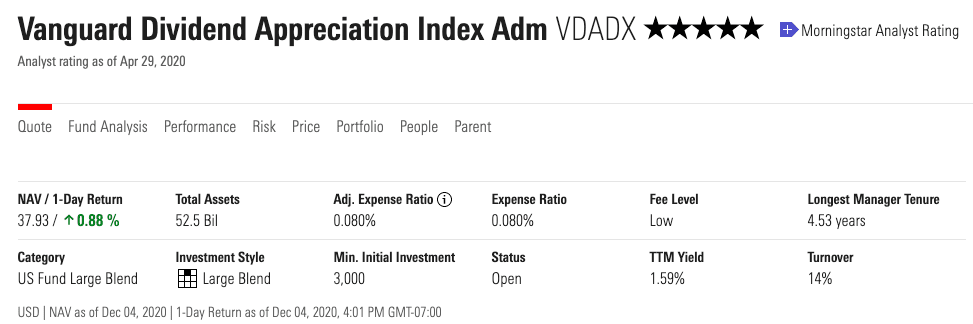

Mutual Fund Price and Category

Lets take a look at what information investors have access to.In this example, we will research the Vanguard Dividend Appreciation Index fund. The fund has a price or Net Asset Value – NAV of $37.93.

The fund’s category is US fund large blend, meaning they are primarily invested in larger companies inside of the United States.

Performance

Here you can see the fund’s performance.

- In 2017, VADAX was up 22.22%.

- In 2018, VADAX was down 2.03%.

- In 2019, VDADX was up 29.68%.

- Year to date | YTD the fund is up 13.70%.

This chart is showing the trailing returns.

- The fund is up 13.70 year to date.

- The fund is up 17.15% for the past year.

- The fund is up 13.64% for the past 3 years.

- The fund is up 14.18% for the past 5 years.

Asset Allocation

Asset allocation reflects the composition of the fund. It shows the percentage the fund that may be invested in stocks, bonds, preferred stocks, cash, or some other security(s).

This is important because if you are an investor that is risk averse, meaning you do not want to stomach potential heavy losses then you may choose to go with a fund that is more heavily weighted in high quality bonds.

If you are an investor that is not risk adverse, then you might consider a fund that leans more heavily towards individual stocks.

If you are an investor that is somewhere in between then you might want to consider a balance fund that has a combination of stocks and bonds or preferred stocks.

In this example, the fund is heavily weighted in U.S. stocks. 99.25% of the portfolio is comprised of U.S. equities, while .72% is in non U.S. stocks.

There is .01% invested in fixed income and .02% is in cash. It is typical to have some cash readily available so that withdrawal requests can be met for the investors.

Top Sectors

Investors can access the top sectors within the fund here. The various percentages of those sectors are displayed at the current rate.

The last column shows the average percentages within that funds categories so that you get an idea of how other similar funds are allocated.

This gives investors instant insight as to how the majority of the fund is being invested.

In this example, consumer defensives has the highest percentage with 17.85%, of the fund currently invested in this sector.

The average for the category is 8.04%

The industrials sector has the 2nd highest percentage within the fund accounting for 15.88% of the fund. Similar funds only allocated 9.92% on average.

Healthcare has the 3rd highest allocation to the fund with 15.51%. The average allocation percentage for similar funds is 14.94%.

The tech sector has the 4th largest allocation percentage with 13.68%, while the industry average is 22.97%

Consume cyclicals are 5th 12.07%. Consumer cyclicals are stocks that are sensitive to the overall health of the economy, such as housing, automotive and retail sectors. This group accounts for 12.07% of the fund, which is close to the industry average of 11.21%.

Top Holdings

Investors also have access to the top individual holdings within a fund.

Here we can see that Walmart is the top holding at 4.58%. Microsoft is 2nd at 4.45%.

This is important information, these stocks have the most impact on the fund.

As an investor, you can monitor the news and financials of these stocks for any potential negative or positive impact that they may have on the fund itself.

The Money Manager(s)

This shows who is managing the fund. Gerard C. Oreilly and Walter Nejman are managing this fund.

Often times a mutual fund manager will manage more than 1 fund. As an investor, do some research on the fund managers.

See how successful they have been by checking the track records of the fund(s) that they are managing.

Fees

One of the main downsides of mutual fund investing are the various fees associated with them.

These fees cut into profits and can drastically reduce the rate of return.

The expense ratio is one of the main fees associated with mutual funds. It is a recurring annual fee that covers expenses associated with the fund.

12b-1 fees are a portion of the expense ratio. It covers expenses such as, marketing materials for tv commercials and advertisements. It also covers management and administrative related expenses.

In this example, the expense ratio for VDADX is .08% for 2020. This expense ratio is low compared to its peers. Why pay higher fees when you do not have to?

The category average is .925%.

The 2nd major expense is Sales Fees.

This chart shows that this is a no load fund, since there is no front load to buy the fund and there is neither a deferred load, nor a redemption load to sell the fund, which is a major plus in the mutual fund world.

Minimum Requirements

Mutual funds can have minimum investment requirements up to about $3000.

In this case, there is a $3000 requirement for standard taxable mutual fund and brokerage accounts. Subsequent purchases drops down to just a $1 requirement.

Typically, there is no minimum requirement for retirement accounts such as IRAs and Roths.

Sometimes funds get closed down or are closed to new investors. VDADX is open to all investors, including new ones.

Most institutional funds require a minimum investment amount of at least $100,000.

Most hedge funds have a minimum requirement between $500,000 – $1 million.

Mutual Fund Classes

Class A

If an investor buys a mutual fund that is classified as class A then you will pay a sales load right when you buy the fund. This sales load is usually between 3% – 6%. So if a fund charges a sales load of 6% and your initial investment is $10,000, then $600 is immediately deducted out of your account.

You still have to pay the annual expense ratio, but this expense ratio is lower for class A than it is for class B or class C.

If you plan on holding onto the fund long term then class A is the best option due to the lower annual expense ratio.

Class B

If an investor buys a mutual fund that is classified as class B, then the investor might have to pay a fee when the fund is sold, on the back end. This is because there is a schedule associated with class B shares.

For example, a mutual fund has a 6 year schedule. If that fund is sold within the 1st year there may be a 6% sales charge.

If the fund is sold between years 1 and 2 of holding the fund then that sales charge would be reduced to 5%.

If the fund is sold between years 2 and 3 of the initial date of purchase then that sales charge would be reduced even further to 4%.

If the fund is sold between years 3 and 4 then the sales charge would be 3%.

If the fund is sold between years 4 and 5 then the fee would be 2%.

If the fund is sold between years 5 and 6, the fee would drop to just 1%.

Finally, if the fund is sold after the 6 year anniversary date of the original purchase then there is no longer a sales fee.

Class B is not the best option if you plan on holding the fund for the long term since the annual expense ratio is higher than the class A counter part. This is ideal for medium term timeframes such as 5 – 10 years.

Class C

Class C mutual funds do not have a front end load or fee when you purchase the fund but has a phased out back end load | sales fee, similar to class b shares.

This back in fee is usually 1% or 2% and is no longer applicable after 1 or 2 years depending on the fund.

If you are an investor and you are planning to sell the fund within 3 years then class C is your best option to minimize the fees.

Class D

Class D mutual funds offer a no load alternative to mutual fund investing, plus the expense ratios tend to be on the lower end of the spectrum relative the other share classes.

Class D funds are not as common as the other classes but they are offered by mutual fund companies in order to offer a more affordable alternative to mutual fund investing.

Class R

R shares is a class of mutual funds designated for employer sponsored retirement accounts such as 401k plans. There is no load to buy or sell these types of funds however, they still have annual expense ratios.

Class I, X, Y, Z

Class I, class X, class Y, class, Z mutual funds are institutional funds that are only available to institutions such as pension funds, 529 plans, non-profit foundations, and retirement plans for corporations.

The expense ratios tend to be much lower than the other classes in order to lure the big money to them. These type of funds often have high minimums in order to purchase them, usually $100,000 and up.

Mutual Fund Exchanges

So what happens if you are not happy with the performance of your mutual fund and you are worried about getting hit with fees if you sell?

I will let you in on a secret, exchanges. An exchange is when you sell one mutual fund for another within the same fund family.

Technically you are selling one fund and buying another but the investor is not being charged a sales load for the transaction.

Another benefit to the investor is that the the initial date of purchase remains in tact even if you do an exchange.

So if there is a 6 year holding period and an investor does an exchange at year 2 of the initial purchase date, the investor is still at year 2 in the holding cycle. The cycle does not start over again.

Brokerage Availability

Once you’ve done your research and figured out which fund that you are interested in purchasing. Now you have to find out if your brokerage firm or mutual fund company offers that particular fund.

If your brokerage firm does not offer that particular fund, you can establish an account with the mutual fund company directly and hold the fund there.

Some mutual fund companies specialize in certain areas. Be sure to check those out.

Final Thoughts

Mutual Funds can be a good way for new investors to take part in the markets.

As a former mutual fund specialist for Merrill Lynch, I wanted to give an in depth analysis of them and to make sure investors are aware of the pros and cons of mutual fund investing.

Some of the pros that we discussed was instant diversification.

If a company within a sector goes bankrupt it is not nearly as big of an issue when you have a bunch of other companies that you are also invested in to help maintain the value of the fund.

We talked about getting access to professional money management and how to research a fund managers track record.

We also talked about how to research a funds performance relative to its peers.

These were some of the pros to mutual funds but we also looked at some of the cons.

The biggest disadvantage to mutual fund investing are the fees associated with mutual funds.

Mutual funds have annual expense ratios that take away from profits.

Many mutual funds have sales loads. Some sales loads can be as high as 6%.

We reviewed the various share classes and the fee structures associated with those classes.